Find Your

Find Your

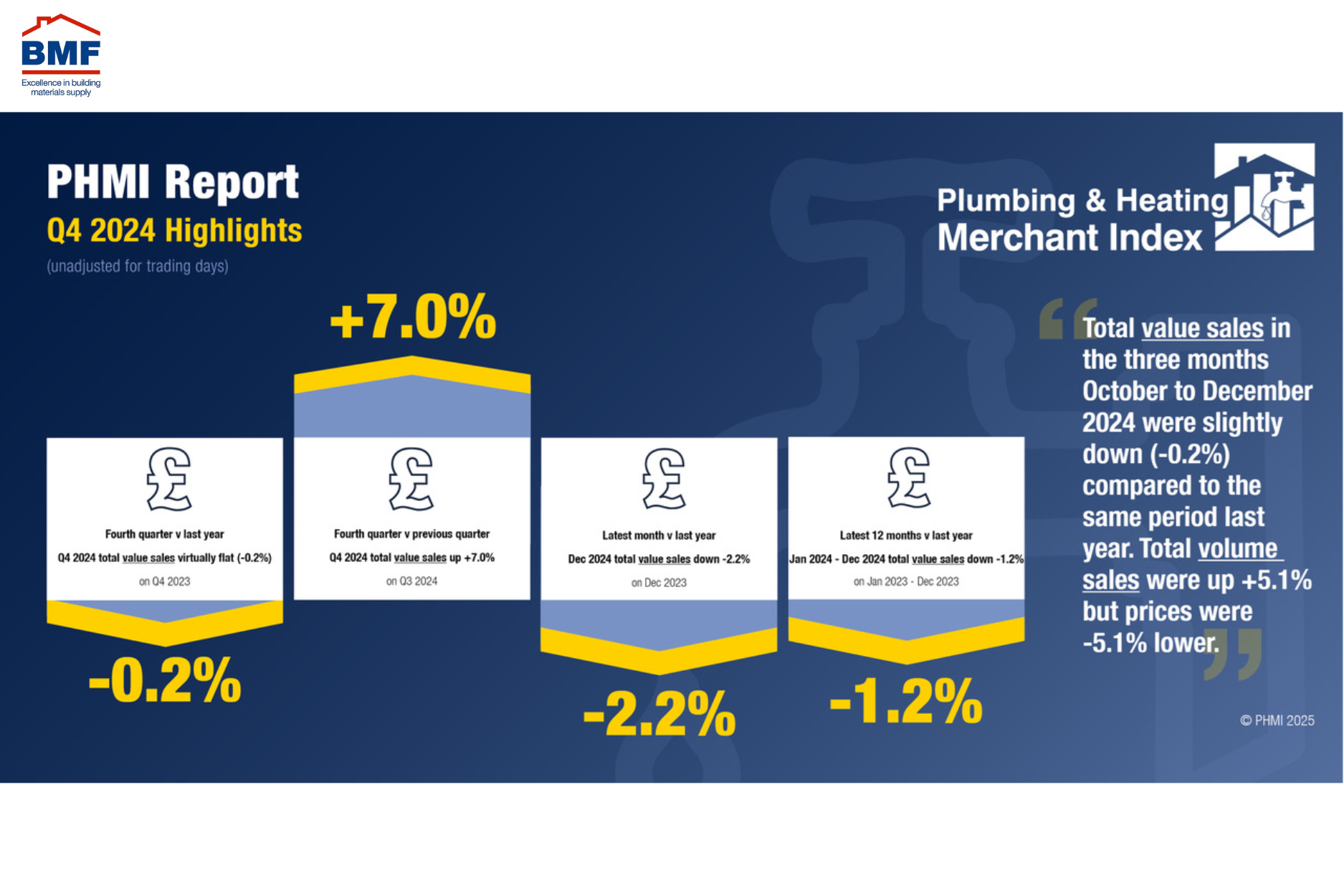

Figures released by the BMF (Builders Merchants Federation) in the Plumbing and Heating Merchants Index (PHMI) for the final quarter of 2024 indicate growing stability in the market, which may be a precursor to positive growth in 2025.

Quarter 4 2024 v Quarter 4 2023

Total value sales in the three months October to December 2024 were virtually flat (-0.2%) compared with the final three months of 2023. Volume sales were up by +5.1% but prices were -5.1% lower.

There was one more trading day in Q4 2024. Like-for-like sale, which take trading day differences into account, were down by -1.9%.

Quarter 4 2024 v Quarter 3 2024

Total value sales in Q3 2024 were +7.0% higher compared with the previous three months, July to October 2024. However, this was driven by price as volume sales fell by -2.6% while prices were +9.9% higher.

With three more trading days in the third quarter, like-for-like sales were -0.8% lower than the second quarter of the year.

Year-on-Year 2024 v 2023

(January – December 2024 v January – December 2023)

Looking across the full year, total value sales in 2024 were down -1.2% compared with 2023. Volume sales were up by +2.2%, but prices were down by -3.3%.

With three more trading days during the last period, like-for-like sales were -2.4% lower.

The data for the PHMI is taken solely from P&H specialists, including City Plumbing Supplies, James Hargreaves Plumbing Depot, Plumbfix, PTS, Williams & Co, and Wolseley, who form part of NiQ GfK’s Plumbing & Heating Merchants Panel, and there is no overlap or double counting between the PHMI and the BMF’s established Builders Merchants Building Index which analyses sales at generalist merchants.